Why This Distinction Matters

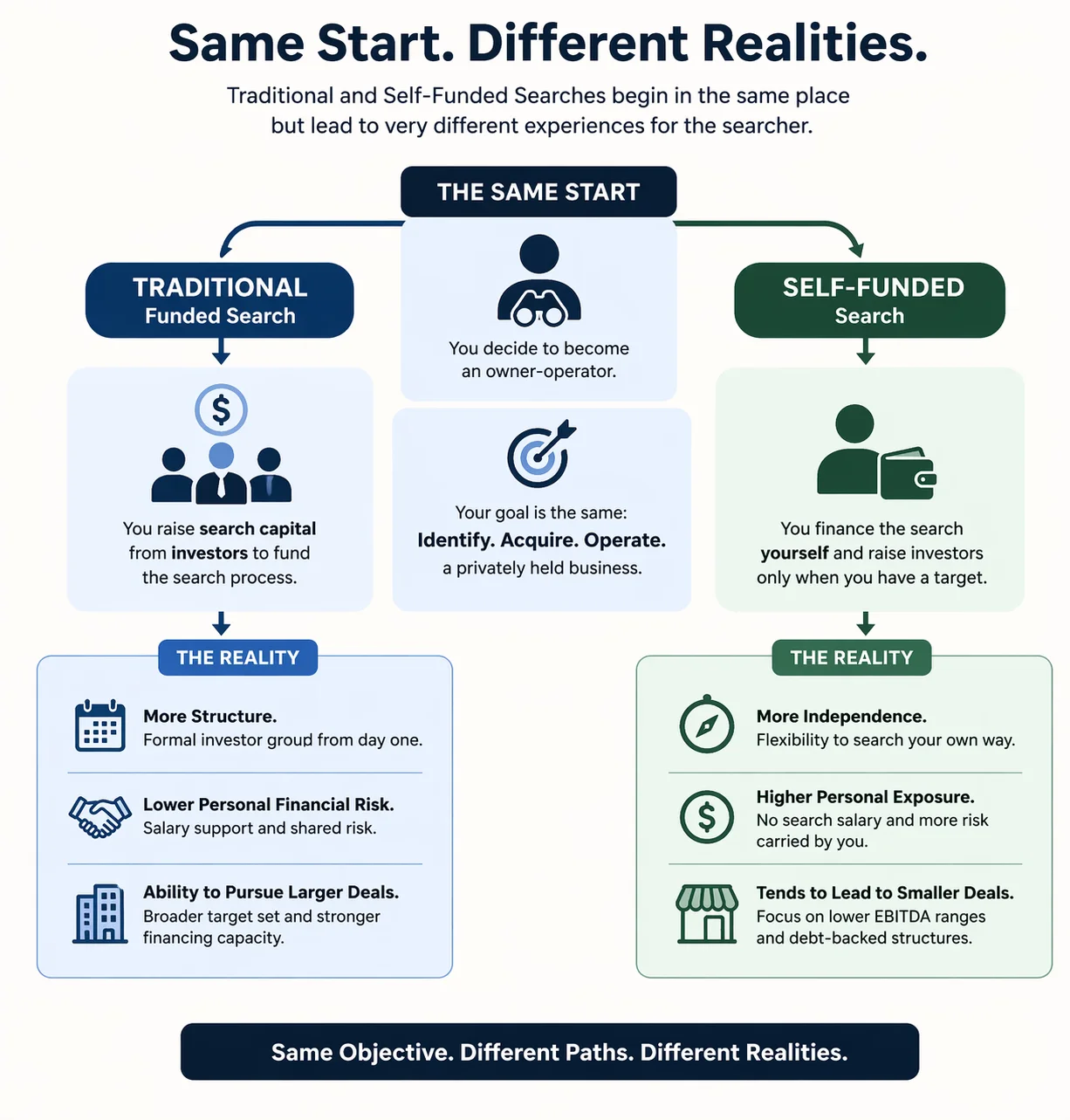

The search fund ecosystem now includes more than one path to becoming an owner-operator. The two most common are the traditional funded search and the self-funded search. Both are built around the same ultimate objective: identifying, acquiring, and operating a privately held business. But in practice, they create very different realities for the searcher.

Stanford’s 2024 study suggests that self-funded searches tend to operate with different economics from the outset: the searcher undertakes the cost of the search personally, works with a smaller and less formal investor base, often uses more debt at acquisition, and usually targets smaller companies while retaining more equity [1]. Taken together, these differences shape the pace of the search, the type of business that can realistically be acquired, the amount of equity the entrepreneur may retain, and the degree of investor involvement.

On the other hand, in a traditional search fund, one entrepreneur or a small team typically raises approximately $300,000 to $750,000 in search capital up front to cover a modest salary and the core expenses of conducting a full-time search [2]. By reducing the searcher’s direct financial burden and creating an investor group from the beginning, the traditional model usually offers a more structured search process and a different risk profile.

What a Traditional Search Fund Actually Looks Like

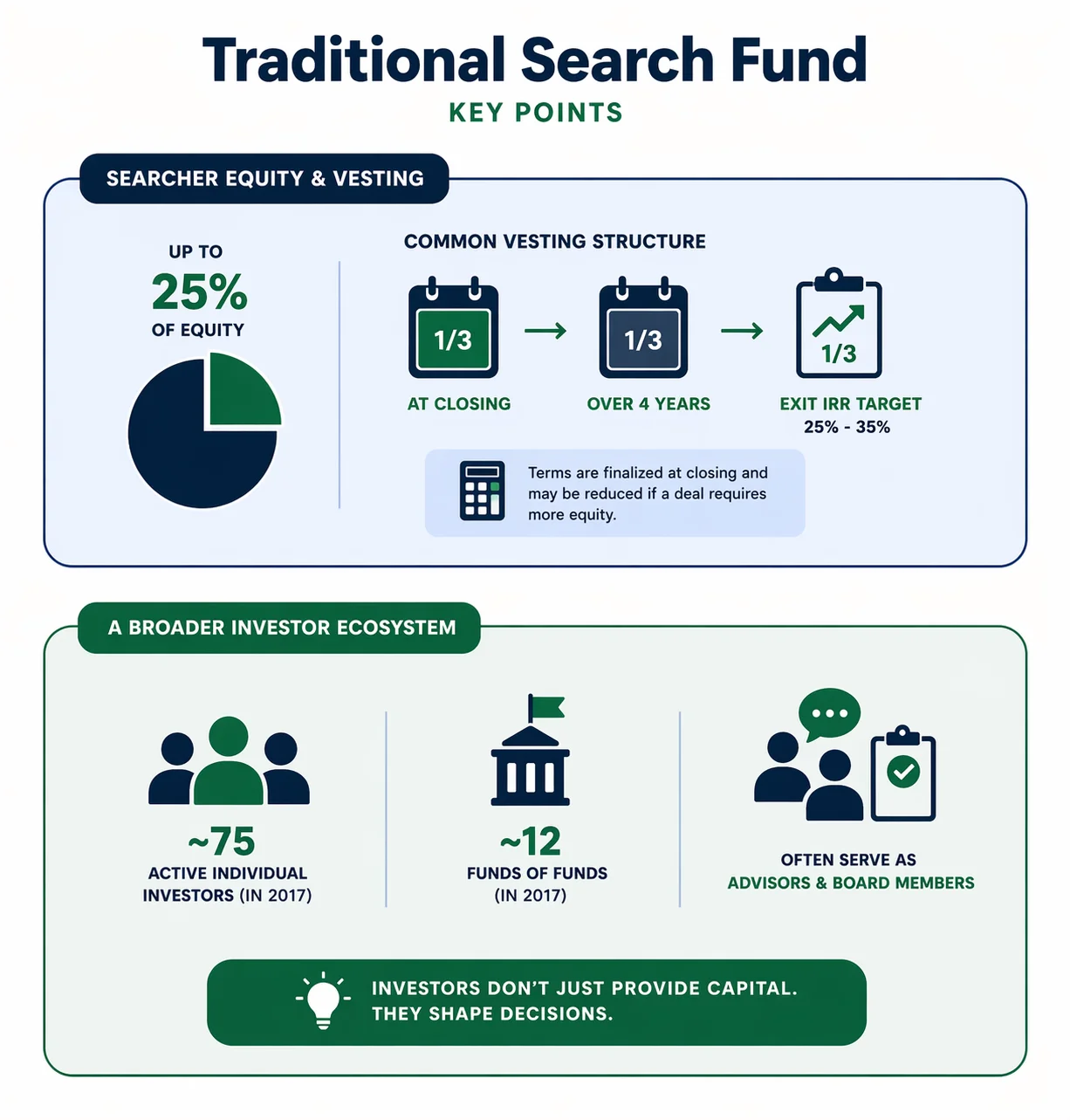

Traditional search defines the searcher’s economic upside in a more formal way. Sharpe notes that the searcher may earn up to 25% of the equity, with that ownership commonly vesting in stages: one-third at closing, one-third over the following four years, and one-third tied to achieving an exit IRR target in the 25% to 35% range [3]. He also notes that these terms are finalized when the acquisition closes and may be reduced if the deal requires a larger equity raise. In practice, this means the traditional model can offer meaningful upside, but that upside is not immediate or automatic. It is structured, performance-linked, and shaped by the economics of the eventual transaction.

Traditional search as a model supported by a broader investor ecosystem rather than a single capital event. In his account of the market at that time, there were approximately 75 active individual investors in the space, along with around a dozen funds of funds, and these investors often participated on common terms while also serving as board members or advisors depending on their experience and availability in 2017 [3]. That matters because, in a traditional search, investors do not simply provide capital. They may also influence governance, diligence, and decision-making as the process unfolds. This is one of the clearest ways the model differs from looser search structures: the capital base often comes with an operating network around it.

What a Self-Funded Search Actually Looks Like

In a self-funded search, the entrepreneur does not raise outside capital to support the search period. Instead, the searcher absorbs the cost of searching personally and brings investors together only when a live acquisition opportunity is ready to be financed. That sounds like a simple capital difference, but it reshapes the economics of the entire process. Because self-funded searchers are not drawing a salary during the search and often rely on higher debt levels at close, they tend to pursue materially smaller businesses than funded searchers [1]. Stanford notes that self-funded searchers often target smaller companies, use more debt in the acquisition, and frequently end up with 50% to 70% ownership of a smaller company.

Yale’s overview of search fund structures pushes the contrast further. It notes that self-funded entrepreneurs often search without salary support. Self-funded searchers may rely on bank debt, seller debt, and a smaller amount of personal equity, and in many cases use SBA 7(a) loans for smaller acquisitions [2]. That is one reason self-funded search is often associated with tighter deal sizes, more constrained capital structures, and greater direct exposure for the operator.

The Real Trade-Off: Risk Transfer vs. Ownership Retention

At a high level, the choice between traditional and self-funded search is not really about which model is better. It is about where risk sits and how reward is shared.

Traditional search shifts part of the early financial risk away from the entrepreneur. The searcher typically benefits from salary support, an investor group formed early in the process, and a more structured path toward financing a larger acquisition. The trade-off is economic dilution and a more formal accountability structure. Investors are involved earlier, and the searcher’s path is usually more collaborative from day one. On the other hand, self-funded search pushes the structure in the other direction. It preserves more independence and can lead to higher ownership if a deal is completed successfully. But that additional upside comes with a heavier burden during the search itself: no salary support, less formal backing, greater exposure to broken-deal costs, and less room for error if financing becomes difficult.

Jim Stein Sharpe frames this choice in practical terms, emphasizing the trade-off between having financial support during the search and retaining more equity after the acquisition [3].

How the Models Affect the Type of Deal You Can Buy

One of the most important differences between the two models is the size and financing profile of the businesses they tend to target.

Traditional searches are generally better positioned to pursue larger companies because the entrepreneur has already assembled an investor base and can often raise acquisition equity more efficiently once a target is found. In the funded model studied by Stanford, the median purchase price for acquired companies in the 2022-2023 was $14.4 million [1].

On the other hand, Yale describes self-funded acquisitions as commonly involving businesses with roughly $500,000 to $1.5 million EBITDA range, while also giving the operator more control over the search. It allows for a more focused strategy by geography, industry, or personal preference, supports the use of SBA 7(a) loans and higher debt levels, and can be accessible to a wider range of searchers than other search fund structures [2]. That does not make the opportunities worse. In many cases, it simply means the acquisition path is more debt-sensitive, more operator-dependent, and less buffered by institutional capital.

This difference matters because many first-time searchers underestimate how much their model choice shapes their target universe. A search thesis is not only an industry choice or a geography choice. It is also a financing choice.

Which Model Fits Which Searcher?

Traditional search is often a better fit for entrepreneurs who want to search full-time within a more structured environment. It tends to suit searchers who value early investor support, a more formal process, and a clearer path toward pursuing larger acquisitions. For many, the appeal is not just reduced personal financial pressure, but also having more guidance and a stronger support system from the beginning.

Self-funded search tends to fit entrepreneurs who want more control over how the search is conducted and are comfortable operating with less formal support. It can be more attractive to searchers who value flexibility in geography, industry, and pace, and who are willing to accept more personal exposure in exchange for potentially higher ownership if a deal is completed successfully.

In the end, this is not only a capital decision. It is also a decision about working style, risk tolerance, and the kind of acquisition path the searcher is prepared to take on.

Conclusion

Traditional and self-funded search funds are built around the same ultimate goal: acquiring and operating a private company. But the two models create very different search experiences. Traditional search usually begins with outside capital, a defined investor group, and a more formal structure around the search itself. Self-funded search, by contrast, places more of the burden directly on the entrepreneur and typically offers greater flexibility in how the search is conducted, how narrowly it is focused, and how much ownership the searcher may ultimately retain.

Those structural differences matter because they shape far more than funding mechanics. They influence the size and type of business a searcher is likely to pursue, the amount of investor involvement present throughout the process, and the level of financial and operational pressure the entrepreneur must carry before a deal is completed. Traditional search tends to offer more support, a more institutional path, and a clearer route toward larger acquisitions, while self-funded search tends to offer more control, more independence, and a more direct connection between the searcher and the economics of the final deal.

For that reason, the distinction between traditional and self-funded search should be understood as a strategic choice, not just a financial one. It affects how the search unfolds, how risk is absorbed, and what kind of ownership journey becomes possible. For entrepreneurs considering the search path, understanding this distinction is essential to choosing the structure that best aligns with their goals, constraints, and preferred way of operating.

Sources

[1] Stanford Graduate School of Business, 2024 Search Fund Study: Selected Observations.

[2] Yale School of Management, Exploring Various Search Fund Structures.

[3] Jim Stein Sharpe, Funding the Search.

* This article combines directly sourced statements with editorial synthesis prepared by the SFP team. Where specific data points, definitions, or practitioner benchmarks are cited, they are drawn from the sources listed above, and more. Other passages reflect interpretation, analysis, and structured commentary informed by those same materials.

Editorial Note

This article combines directly cited source-based statements, paraphrased material derived from the sources listed above, and editorial synthesis prepared by the SFP team. Where definitions, factual claims, or data points are directly attributable to a source, they are cited accordingly. Other passages reflect analytical reframing, interpretation, and structured commentary based on the same source base. Given the limited number of authoritative sources on certain aspects of this topic, some uncited language may still resemble commonly used formulations in the broader search fund literature, even where the final wording has been independently written or adapted for editorial clarity.