Why LMM Matters in Search

Search funds are built around the acquisition of a single business [1] that a searcher can buy, lead, and grow over time. That basic structure matters because it immediately narrows the part of the private-company universe that is realistically relevant. Searchers are usually not pursuing very large, broadly intermediated assets. They are more often focused on companies where ownership transfer, operational leadership, and long-term value creation can still be shaped directly by the searcher.

That is why the lower middle market matters so much in search. It is the part of the market where a company can be substantial enough to support a real acquisition and leadership transition, yet still small enough for a searcher’s judgment, persistence, and operating role to make a meaningful difference. For searchers, this is not just a market-size label. It is the segment where the search fund model becomes most practical.

What the Lower Middle Market Means in a Search Fund Context

There is no single universal definition of the lower middle market, which is one reason weaker articles on the topic often become vague or repetitive. Different market participants define the segment differently depending on whether they emphasize revenue, EBITDA, enterprise value, or buyer profile. In a search fund context, however, the more useful question is not where the category begins or ends in abstract terms. The more useful question is where the model actually fits.

In practice, the lower middle market refers to the part of the private-company universe that sits below the scale typically associated with large private equity transactions, but above the level where a business may be too small, too unstable, or too informal to support a credible ownership transition. That is the part of the market where searchers most often operate, because it is often where a business is large enough to support an acquisition and leadership transition, yet still small enough for hands-on ownership to matter in a meaningful way.

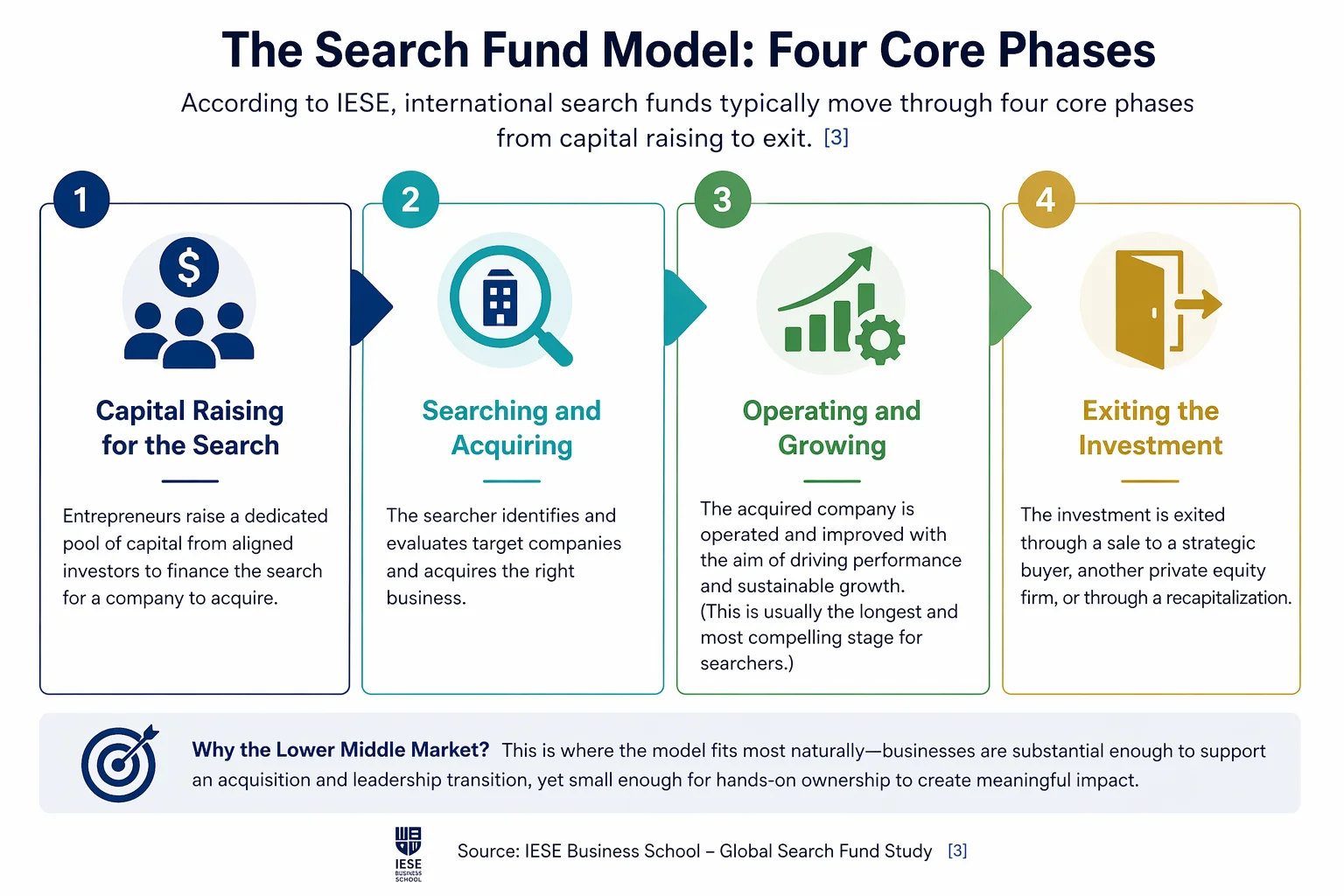

This alignment becomes clearer when the structure of the model itself is considered. According to IESE, international search funds typically move through four core phases: capital raising for the search itself, identifying and acquiring a company, operating and growing the acquired business, and ultimately exiting the investment [3]. In practice, the lower middle market is often where that sequence becomes most feasible.

Why Search Funds Gravitate Toward This Segment

Search funds are designed for direct ownership and hands-on leadership, not passive exposure. Searchfunder defines a search fund as an entity created to acquire a single business, and notes that searchers are often first-time CEOs supported by experienced investors and advisors [1]. IESE describes search funds as a path for young entrepreneurs to become equity-owning CEOs while investors support them in their first CEO roles [2]. Those are not minor details. They explain why the model is structurally drawn toward businesses where new leadership can matter in concrete operational ways.

IESE argues that search funds operate in a fragmented part of the market where deals are often too small for institutional investors and too large for most angel groups [4]. That helps explain why the lower middle market is such an important context for search: it is often where ownership transition, operational leadership, and acquisition feasibility align most clearly. At one end of the spectrum, very large companies may be less suited to the model because they typically require a more institutional transaction and ownership environment. At the other end, very small businesses may be harder to acquire and scale within a search-fund framework, particularly when they offer limited infrastructure or operating depth. The lower middle market often sits between those two extremes, which is one reason it remains one of the most practical contexts for understanding how search funds actually work.

Fragmentation, Succession, and the Searcher Opportunity

What makes the lower middle market especially relevant is not only size, but structure. Many businesses in this segment are often owner-led, privately held, and built over long periods rather than designed from the outset for institutional ownership. That can create a market characterized by fragmentation, uneven levels of professionalization, and inconsistent visibility across targets.

For searchers, that matters because differentiated access may still come from disciplined sourcing, sustained outreach, and the ability to build credibility directly with owners. This does not make the market easier. It makes execution more dependent on process quality, search discipline, and judgment.

Succession is also an important part of the picture. Many businesses in this segment may be stable companies whose owners are thinking about transition, continuity, or partial liquidity after years of operating the business themselves. That profile can fit the search model well, because the buyer is not only offering capital, but also a credible path forward for the company.

Why Process Discipline Matters in the Lower Middle Market

The lower middle market is often described as opportunity-rich, but that phrase can be misleading if it is left undefined. A large target universe does not automatically translate into accessible opportunities. In practice, searchers may need to review many companies, return to the same market repeatedly, and work through extended periods of uncertainty before identifying a target worth pursuing seriously.

That is why process discipline matters so much. In this part of the market, advantage may come less from spotting a single exceptional opportunity and more from building a repeatable system for identifying, organizing, comparing, and revisiting targets over time. The lower middle market tends to reward searchers who can combine conviction with structure. It is a broad, fragmented, and often uneven market. Without disciplined execution, much of its apparent opportunity can remain difficult to convert into real deal flow.

Conclusion

The lower middle market matters in search funds because it is where the model becomes operationally realistic. It contains the kinds of businesses that are often large enough to support an acquisition and leadership transition, but still small enough for a searcher’s personal involvement to matter directly.

More importantly, it is not just a company-size category. It is a market environment shaped by fragmentation, succession, private ownership, and uneven institutional coverage. That is precisely why search funds tend to operate there. The model is built for buyers who are prepared to search patiently, evaluate carefully, and lead actively after acquisition. Therefore, understanding the lower middle market is therefore not a side topic within search. It is part of understanding the search fund model itself.

Sources

[1] Searchfunder, “What is a search fund?”

[2] IESE Business School, International Search Fund Center.

[3] IESE Insight, “Search funds asset class maintains global growth.”

[4] Search Funds - What Has Made Them For?, https://www.iese.edu/media/research/pdfs/ST-0357-E.pdf

Editorial Note

This article combines directly cited source-based statements, paraphrased material derived from the sources listed above, and editorial synthesis prepared by the SFP team. Where definitions, factual claims, or data points are directly attributable to a source, they are cited accordingly. Other passages reflect analytical reframing, interpretation, and structured commentary based on the same source base. Given the limited number of authoritative sources on certain aspects of this topic, some uncited language may still resemble commonly used formulations in the broader search fund literature, even where the final wording has been independently written or adapted for editorial clarity.