What the Search Process Actually Is

From the outside, the search process can appear simple: identify a company, negotiate a transaction, and step into the CEO role. In reality, the model is far more demanding and usually unfolds over a longer and less predictable timeline than most first-time observers expect. Stanford Graduate School of Business defines a search fund as an investment vehicle through which investors financially support an entrepreneur’s efforts to locate, acquire, manage, and grow a company [2]. That definition is important because it makes clear that search is not just about finding a business. It is part of a broader process of acquisition, leadership transition, and long-term value creation.

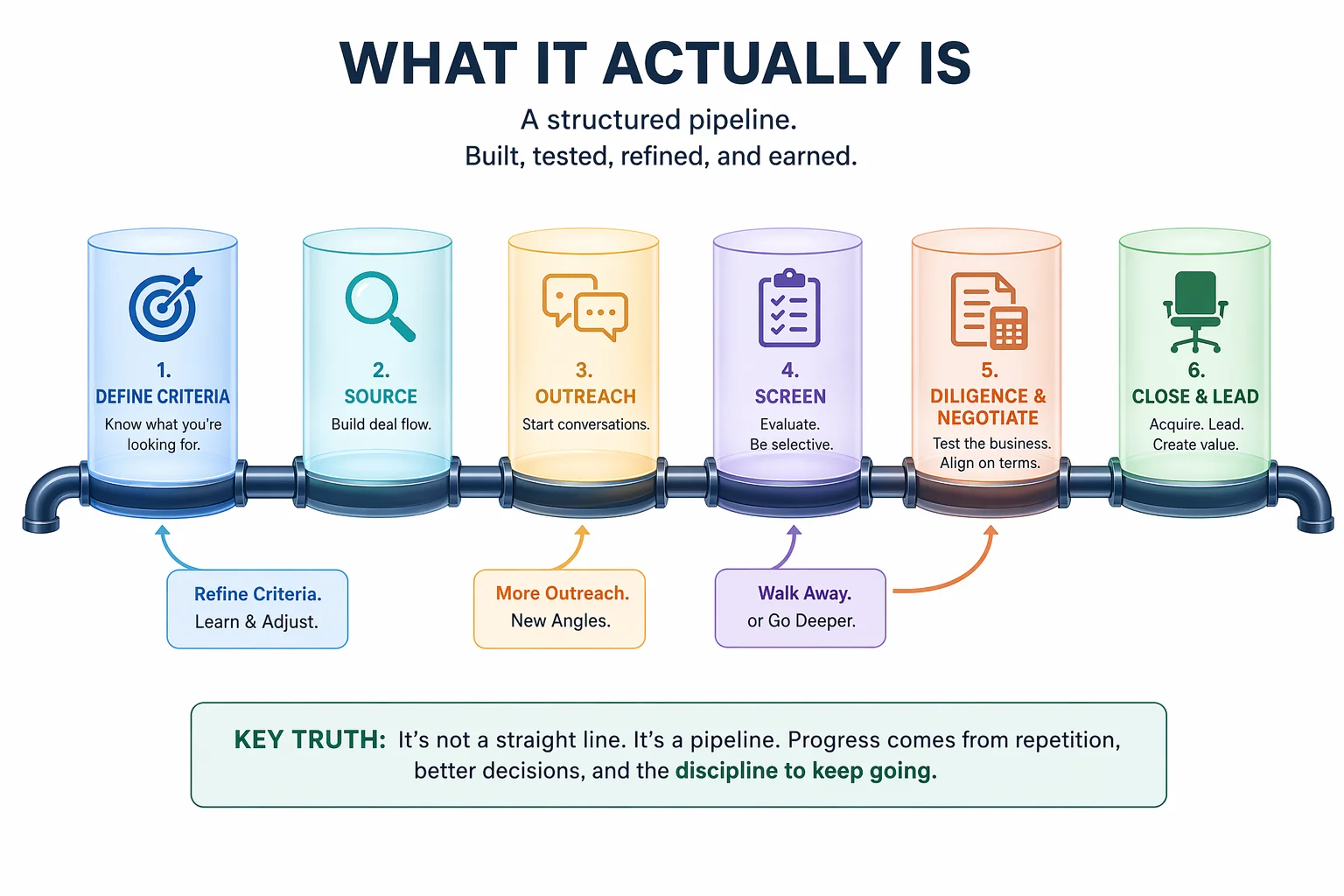

In practice, the search process is best understood as a structured pipeline rather than a straight line. Searchers typically move from defining criteria to sourcing opportunities, conducting outreach, screening targets, negotiating terms, and advancing selected companies into diligence and closing discussions. Each step serves as a filter, reducing noise and increasing selectivity as the process moves forward. For that reason, successful searches are usually built on consistency and process discipline rather than on the hope of finding one perfect opportunity early. Jim Stein Sharpe makes a similar point in practical terms, arguing that if searchers are not making at least 2-3 offers a month, then there is a problem with their searches [4]. Viewed this way, search is not simply a matter of identifying a target. It is a matter of building and sustaining a process that produces enough qualified opportunities to support good decisions.

Why Every Search Starts With Clear Criteria

Serious searches except from industry agnostic ones do not begin with random listings. They begin with a thesis. That usually includes industry focus, geographic scope, revenue and EBITDA range, business model preferences, customer concentration tolerance, and the type of operational complexity a searcher is prepared to take on. This criteria-first approach is widely associated with disciplined search execution because it helps narrow the universe of businesses into a realistic acquisition target set.

Without clear criteria, a search can quickly become reactive. A searcher may review many businesses, but without a defined filter it becomes much harder to separate a genuinely attractive company from one that is simply available. That is one reason experienced operators and advisors consistently stress process discipline early in the search.

How Searchers Build Deal Flow

Once criteria are established, the next challenge is building deal flow. In practice, this often includes broker relationships, targeted industry mapping, inbound referrals, proprietary outreach to owners, and repeated review of smaller-market opportunities. The key idea is that sourcing is not a one-time action. It is a system for producing enough qualified conversations to make selective decisions possible.

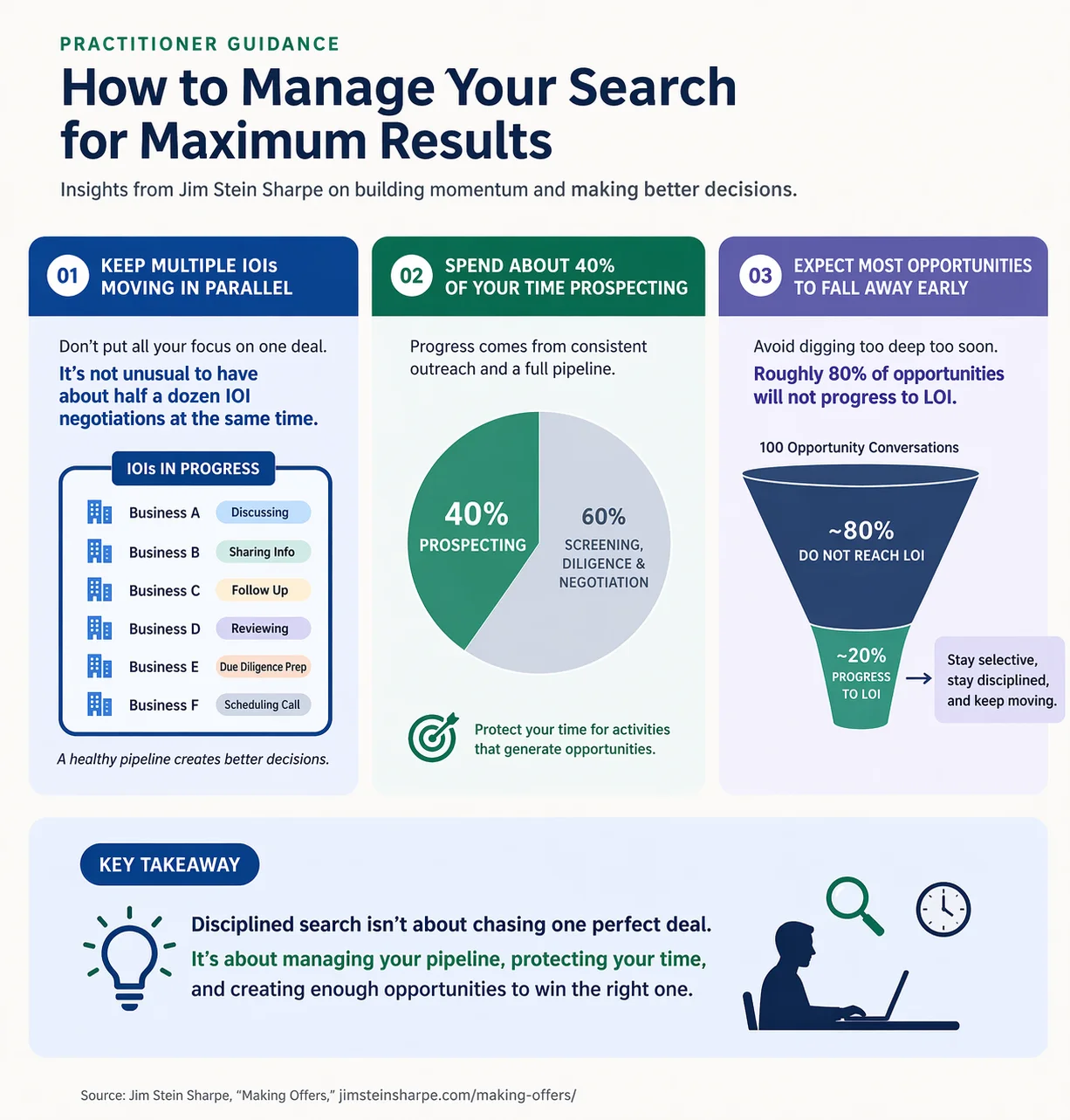

Jim Stein Sharpe writes that making offers “quickly and often” is critical to buying a business and argues that if a searcher is not making at least two to three offers a month, there is likely a problem with the search process [4]. That observation matters because it shifts the focus from passive reviewing to measurable pipeline execution. Practitioner guidance in the search space also suggests that disciplined pipeline management matters as much as judgment on any single deal. Jim Stein Sharpe advises searchers to keep multiple early-stage opportunities moving at once, noting that it is not unusual to have several IOI discussions underway at the same time [4]. He also recommends allocating roughly 40% of search time to prospecting and warns against going too deep too early, since approximately 80% of opportunities will not convert into LOIs [4]. The broader implication is clear: effective searchers do not build their process around one deal, but around a steady flow of qualified opportunities.

Why Proprietary Outreach Matters

Many attractive businesses never reach a broad auction-style or fully intermediated sale process. As a result, proprietary outreach remains a central part of search. Rather than relying solely on listed opportunities, searchers often build deal flow by contacting owners directly, developing relationships over time, and identifying businesses where succession interest may exist before a formal sale is launched. This matters because brokered processes are only one part of the market. By the time a business is widely marketed, multiple buyers may already be reviewing the same opportunity, which can make pricing more competitive and reduce the searcher’s ability to build a differentiated relationship with the seller. Proprietary outreach works differently. It gives searchers a way to start conversations earlier, understand ownership dynamics before a formal process begins, and sometimes access opportunities that would never have appeared in a public listing environment.

In practice, this does not mean every direct outreach effort will produce a deal. The value of proprietary outreach is that it expands the search universe beyond visible listings and allows the searcher to build a pipeline that is not entirely dependent on intermediaries. Over time, that can lead to better market coverage, more direct seller insight, and a stronger understanding of where real transition opportunities may exist. It also helps explain why search is typically more labor-intensive than outsiders expect. The work is not limited to reviewing companies that are already on the market. It also involves generating conversations, qualifying owner interest, and continuously refining the pipeline through repeated outreach and screening. In many cases, the searcher is not just evaluating businesses. The searcher is also trying to understand timing, motivation, succession readiness, and whether an owner is genuinely open to a transaction.

That is why proprietary outreach should not be viewed as a side tactic. In many searches, it is one of the core mechanisms through which opportunities are created, relationships are built, and off-market possibilities are surfaced. For searchers who want broader coverage and more control over their pipeline, proprietary outreach is often not optional. It is foundational.

How Opportunities Are Screened

As opportunities emerge, the process shifts from sourcing to screening. At this stage, the core question is not whether a company sounds interesting, but whether it is understandable, durable, and transferable enough to support a change in ownership and leadership. Financial analysis, business quality, and leadership transition risk begin to matter more than surface-level excitement. This is the point where early interest starts to give way to real acquisition judgment.

Screening usually involves questions about quality of earnings, add-backs, customer concentration, margins, owner dependence, and the overall durability of cash flow. Jim Stein Sharpe’s discussion of offers also highlights how assumptions around EBITDA and add-backs can materially affect whether an opportunity remains attractive under closer scrutiny [4].

Just as importantly, screening is not only about identifying upside. It is also about identifying reasons not to proceed. A company may appear attractive at first because of its size, sector, or reported profitability, yet become far less compelling once the searcher looks more closely at how revenue is generated, how dependent the business is on the owner, or how resilient performance would be after a transition. In that sense, effective screening is both analytical and selective: it helps narrow a broad set of possibilities into a much smaller group of businesses that are not only interesting on paper, but realistic candidates for acquisition.

Why Many Deals Fall Apart

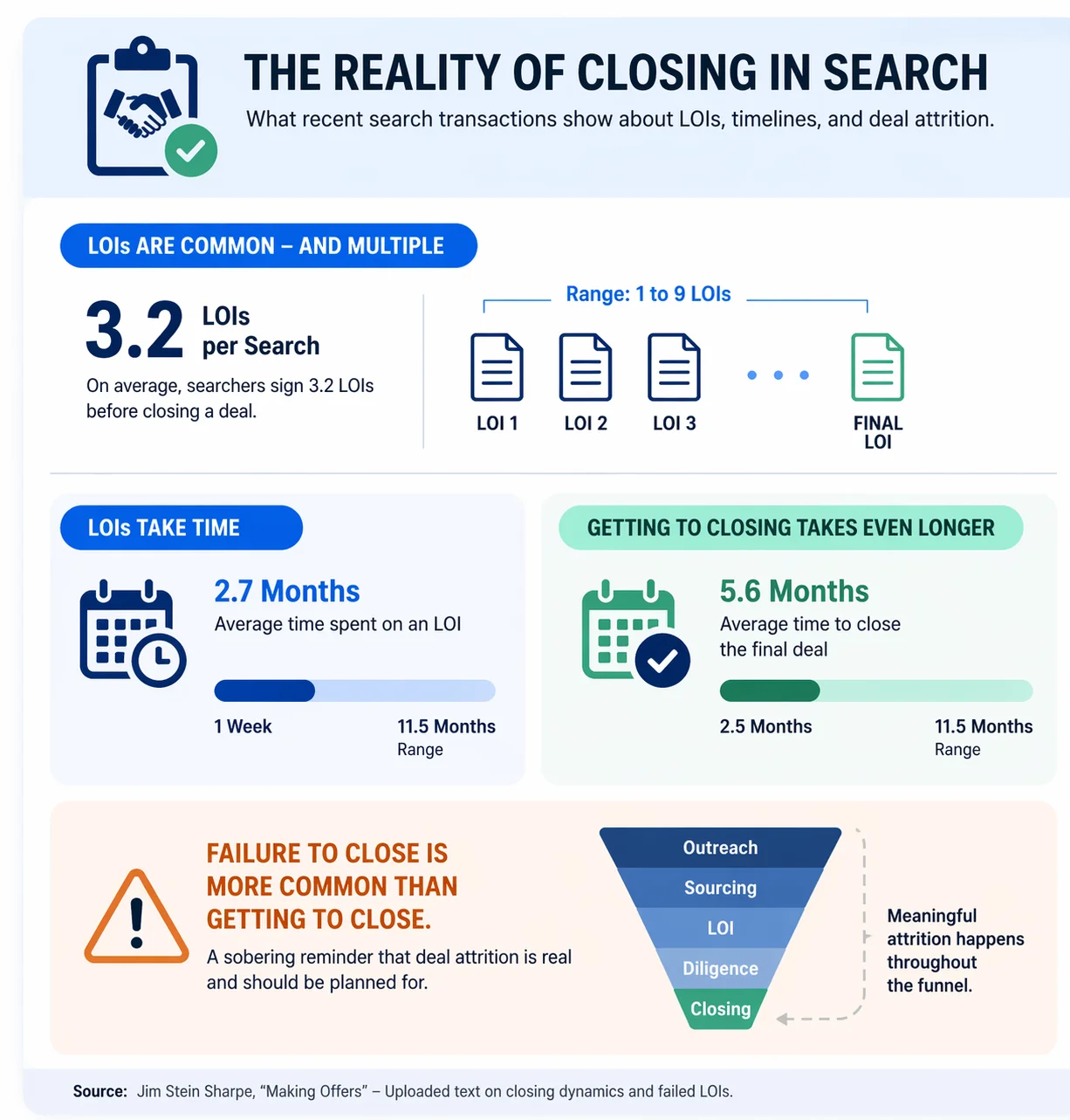

One of the most important realities in search is that promising deals often fail. Sellers may change their minds, valuations may drift, financing may become more difficult, or unexpected issues may emerge during diligence. This is one reason the search process should be understood as a funnel with meaningful attrition rather than a smooth progression from outreach to closing. Practical data from Sharpe, reinforces that point: one review of recent transactions reported an average of 3.2 LOIs per search, an average of 2.7 months spent on an LOI, and an average of 5.6 months to reach closing on the final deal [6]. The same source concludes that failure to close is more common than getting to close, which underscores how much uncertainty remains even after a deal appears promising.

Even after a signed LOI, the process remains highly fragile. Terms that seem manageable early on can become harder to resolve as diligence progresses, financing partners become more involved, and sellers react to the emotional and practical implications of a transaction. In that sense, many deals do not fail because they were obviously weak from the start. They fail because the path from interest to closing is longer, more complex, and more vulnerable to disruption than many first-time searchers expect.

What the Process Means for Searchers, Investors, and Operators

For searchers, the lesson is that persistence matters, but persistence alone is not enough. The searcher also needs clear criteria, a measurable sourcing system, disciplined screening, and enough emotional distance to reject weak deals when the data and structure do not hold up. This conclusion is an inference supported by Stanford’s acquisition data and Jim Stein Sharpe’s emphasis on cadence, metrics, and repeated offer-making.

For investors, the takeaway is that evaluating a searcher should involve more than enthusiasm or background. It should also involve assessing whether the search process itself is well designed, well measured, and sustainable over time. For self-funded searchers and operators, the process is equally relevant because the underlying challenges remain the same: deal flow, selectivity, diligence, negotiation, and the difficulty of getting one good deal done. This is an inference drawn from the search process evidence above.

Conclusion

Search is not just a deal process. It is a test of judgment, consistency, and execution over time. The strongest searchers are not necessarily the ones who see the most opportunities, but the ones who build a process capable of generating, filtering, and advancing the right ones. That process begins with clear criteria, becomes more selective through screening and diligence, and is constantly shaped by the realities of seller behavior, financing, timing, and deal attrition.

Seen this way, the search process is best understood not as a linear sequence, but as a disciplined system. It rewards patience, but not passivity. It rewards conviction, but not fixation. And above all, it rewards searchers who can remain analytical when the process becomes emotional, and selective when the pressure to close begins to rise.

Sources

[1] CFA, Search Funds: A Strategic Investment in Underserved Markets (https://rpc.cfainstitute.org/blogs/enterprising-investor/2025/search-funds-a-strategic-investment-in-underserved-markets)

[2] Stanford Graduate School of Business, 2024 Search Fund Study. (https://www.gsb.stanford.edu/faculty-research/case-studies/2024-search-fund-study)

[3] Stanford Graduate School of Business, 2024 Search Fund Study: Selected Observations.(https://www.onetoonefunds.com/wp-content/uploads/sites/11/2024/10/2024_Search-Fund-Study_Selected-Observations_Stanford-GSB.pdf)

[4] Jim Stein Sharpe, Making Offers. (https://jimsteinsharpe.com/making-offers)

[5] Jim Stein Sharpe, Search Tips. (https://jimsteinsharpe.com/search-tips)

[6] Jim Stein Sharpe, Getting to Closing. (https://jimsteinsharpe.com/getting-to-closing/)

* This article combines directly sourced statements with editorial synthesis prepared by the SFP team. Where specific data points, definitions, or practitioner benchmarks are cited, they are drawn from the sources listed above, and more. Other passages reflect interpretation, analysis, and structured commentary informed by those same materials.

Editorial Note

This article combines directly cited source-based statements, paraphrased material derived from the sources listed above, and editorial synthesis prepared by the SFP team. Where definitions, factual claims, or data points are directly attributable to a source, they are cited accordingly. Other passages reflect analytical reframing, interpretation, and structured commentary based on the same source base. Given the limited number of authoritative sources on certain aspects of this topic, some uncited language may still resemble commonly used formulations in the broader search fund literature, even where the final wording has been independently written or adapted for editorial clarity.