Who Becomes a Searcher?

There is no single template for who becomes a searcher. The search fund ecosystem attracts people from a range of professional backgrounds, though over time some patterns have become visible. Searchers are often people who want to move from analysis into ownership, from advising businesses to operating one, and from structured careers into a path with much more ambiguity and personal responsibility.

Demographic Distribution of Searchers

The table shows that the principals’ background profile has broadened, but not evenly. Demographically, the model still centers on relatively young principals, with a median starting age of 33 in the 2022-2023 cohort and most principals still concentrated in the 30-35 range [7]. At the same time, the age spread is wider than in many earlier periods. The maximum age rises to 57, and the share of principals over 40 reaches 15%, which suggests that search is no longer confined as tightly to a narrow early-career window.

On the other hand, the gender distribution, however, remains strikingly concentrated. Even in the most recent cohort, 93% of reported principals are male and only 7% are female. Female representation was higher before 2002, declined across subsequent cohorts, and only began to recover modestly in more recent years.

![International principals’ background [7]](https://api-help.searchfundplus.com/uploads/articles/article-1776781499182-337708530.webp)

The post-MBA timing data points to a second shift in the ecosystem. Search is still connected to business school pathways, but the model appears less centered on the immediate post-MBA launch than it once was. In the 2022-2023 cohort, only 23% launched within one year of graduation, while larger shares entered one to three years later, four to seven years later, or even eight or more years after business school. Just as importantly, 40% of principals in the most recent cohort had no MBA at all, the highest figure shown in the table. Taken together, this suggests that the search fund path is becoming more flexible both in timing and in educational profile. The MBA remains an important route into the ecosystem, but it no longer appears to define the model as narrowly as it did in earlier cohorts.

That is one reason the question matters. “Who becomes a searcher?” is not only about demographical distinction or educational categories. It is also about what kind of person is willing to spend months, and often years, sourcing companies, speaking with owners, evaluating opportunities, and pursuing a path that may involve long stretches of uncertainty before a deal is ever completed.

On the other hand, the tablo below indicates the international principals’ professional background. The table reinforces a key point in the search fund ecosystem: there is no single professional background that defines a searcher, but certain career paths remain consistently overrepresented. In the 2022-2023 cohort, management consulting was the most common background at 26%, followed by investment banking/finance at 20%, line/general management at 14%, private equity at 10%, and operations at 9%. This pattern suggests that search funds continue to attract individuals from backgrounds that build strong skills in business evaluation, strategic analysis, financial judgment, and operational decision-making. At the same time, the distribution across categories shows that the search fund model is not limited to a narrow finance-only pipeline. Searchers also come from entrepreneurship, engineering, sales, venture capital, law, and other professional tracks, even if these remain smaller shares of the overall principal pool.

Common Backgrounds in the Search Fund Ecosystem

![International principals’ professional background (%) [7]](https://api-help.searchfundplus.com/uploads/articles/article-1776781560978-697994161.webp)

The time pattern in the table is just as important as the most recent cohort. Earlier periods were more heavily concentrated in investment banking/finance and, in some cases, general management, while more recent cohorts appear somewhat more balanced across consulting, finance, management, private equity, and operations. That shift suggests that the professional profile of a searcher has become broader over time, even if it still clusters around analytically careful and commercially relevant fields. From a different perspective, the table supports a clear conclusion: successful searchers do not come from one uniform background, but the ecosystem continues to favor experience that is close to business analysis, investment judgment, leadership, and company evaluation. In other words, the search fund path is becoming more professionally diverse, but its center of gravity still sits in high-intensity, decision-oriented roles.

Why Business Schools Matter So Much in Search

Business schools have played an unusually important role in making the search fund model more visible, more structured, and more teachable. Stanford Graduate School of Business remains one of the field’s central anchors through its Search Fund Primer and recurring Search Fund Study. Stanford describes the search fund as an investment vehicle in which investors back an entrepreneur’s effort to locate, acquire, manage, and grow a private company [1].

Harvard Business School has also institutionalized Entrepreneurship through Acquisition through formal coursework and student infrastructure [3][4]. It is a field course that Entrepreneurship through Acquisition teaches practical skills required to become an effective entrepreneur through acquisition, including screening targets, understanding debt and equity financing sources, due diligence, seller cold calls, and loan negotiation [3]. HBS also maintains an Entrepreneurship Through Acquisition Club whose stated purpose is to educate the HBS community and provide potential searchers with the network and resources needed to succeed [4].

IESE plays a similarly important role internationally. Its International Search Fund Center supports entrepreneurs and investors around the world engaged in search funds, and it has tracked international search funds since 2011 in conjunction with Stanford GSB while publishing a biennial report on international search fund results. [5][6]

What matters here is not only that leading business schools teach search. It is that they helped give the search fund model structure, language, and legitimacy. Through research, Entrepreneurship through Acquisition coursework, and network formation, these institutions made the search path more visible to aspiring principals and more understandable to the broader market. That is why business schools matter so much in search: they did not just describe the model, they helped build the search fund ecosystem around it.

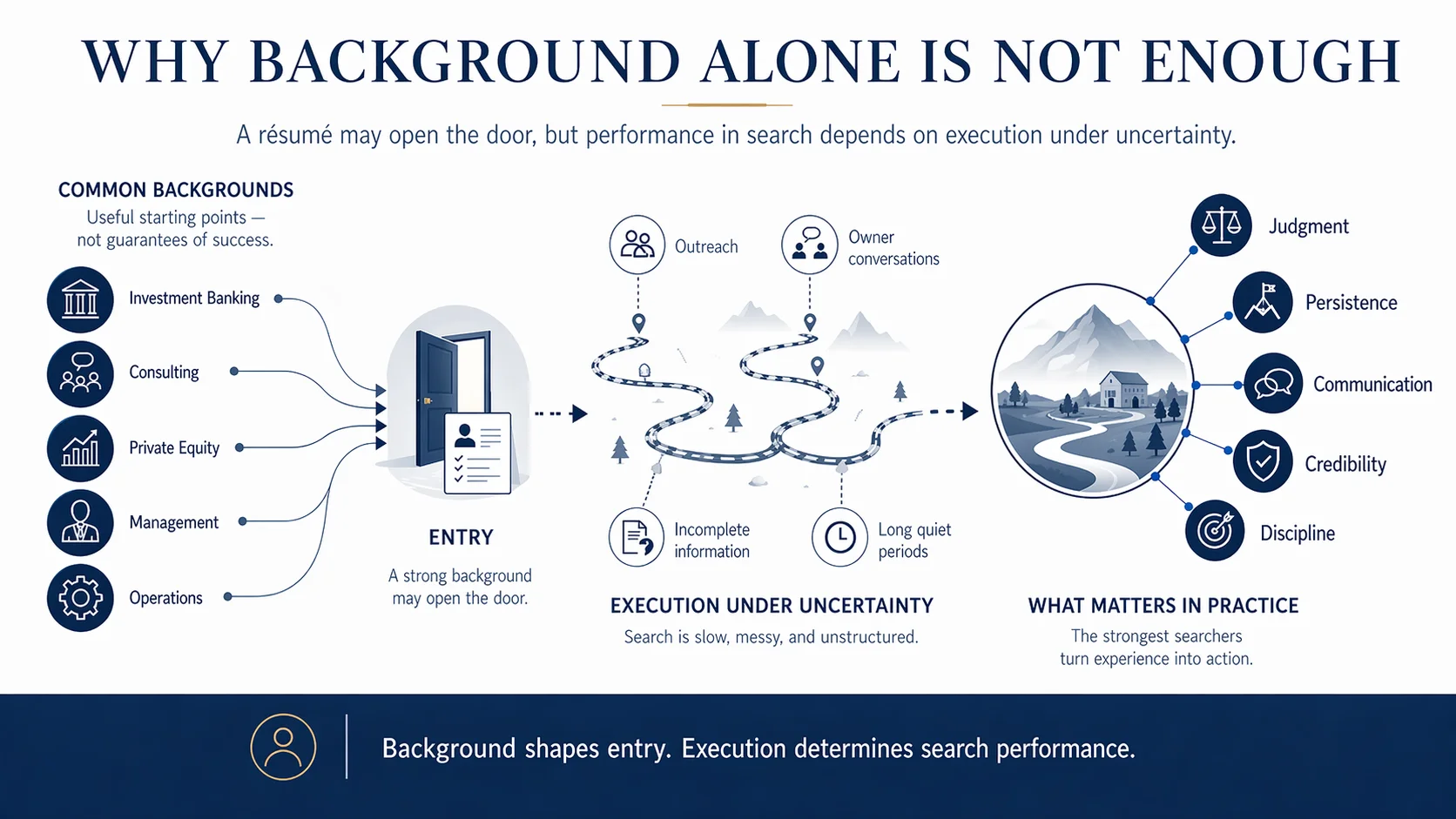

Why Background Alone Is Not Enough

A strong résumé may open the door in search, but it does not determine who will perform well once the process begins. The search fund path is not simply a finance exercise, nor is it just a sourcing function. It requires a combination of market judgment, persistence, communication skill, and readiness for eventual ownership. That is why background matters, but only up to a point.

The deeper challenge of search is execution under uncertainty. Someone may come from investment banking, consulting, private equity, or management and still find the process difficult in practice. Search demands repeated outreach, real conversations with owners, decisions made with incomplete information, and the patience to keep working through long periods where little appears to be happening. The issue is not only whether a person can evaluate a business. It is whether they can sustain credibility, discipline, and forward motion when the path is slow, messy, and unstructured.

That distinction matters because the search fund ecosystem does not reward pedigree in isolation. It rewards the ability to turn experience into action. The strongest searchers are usually those who can combine analytical diligence with emotional steadiness, seller-facing credibility, and the discipline to continue searching even when momentum is weak. Background may shape entry into search, but it does not by itself predict search performance.

What Actually Makes Someone a Strong Searcher

The strongest searchers are usually people who combine analytical discipline with entrepreneurial stamina. They need enough financial and commercial judgment to evaluate a business seriously, but they also need the endurance to continue when outreach goes nowhere, sellers change direction, or promising conversations fail to become actionable opportunities.

Interpersonal credibility matters just as much. Many founders are not simply comparing price. They are deciding whether the buyer seems trustworthy, capable, serious, and prepared to carry the business forward responsibly. In practice, this means strong searchers often stand out not because they have the flashiest background, but because they can stay organized, communicate clearly, build trust with owners, and keep moving through ambiguity without losing process discipline.

So who becomes a searcher? In surface terms, many come from consulting, finance, private equity, and management roles. In deeper terms, search tends to attract people who want to become owner-operators and are willing to accept the uncertainty, persistence, and personal accountability that come with that transition.

Conclusion

The best way to understand who becomes a searcher is not to look for a single résumé pattern. The search fund world clearly draws from certain professional pools, and business schools have helped make those pathways more visible and more structured. But the model does not reward background alone.

What matters more is fit with the work itself. Search favors people who can move from analysis into action, from interest into commitment, and from professional credibility into seller trust. In that sense, the real dividing line is not whether someone came from banking, consulting, or operations. It is whether they are genuinely prepared to search with discipline and eventually lead with ownership.

Sources

[1] Stanford Graduate School of Business, Search Funds

[2] Stanford Graduate School of Business, Search Funds and 2024 Search Fund Study

[3] Harvard Business School, Field Course: Entrepreneurship through Acquisition

[4] Harvard Business School, Entrepreneurship Through Acquisition Club

[5] IESE Business School, International Search Fund Center

[6] IESE Business School, International Search Funds–2022

[7] IESE Business School, International Search Funds–2024

Editorial Note

This article combines directly cited source-based statements, paraphrased material derived from the sources listed above, and editorial synthesis prepared by the SFP team. Where definitions, factual claims, or data points are directly attributable to a source, they are cited accordingly. Other passages reflect analytical reframing, interpretation, and structured commentary based on the same source base. Given the limited number of authoritative sources on certain aspects of this topic, some uncited language may still resemble commonly used formulations in the broader search fund literature, even where the final wording has been independently written or adapted for editorial clarity.